by

by Health insurance has become one of the most important financial tools for individuals and families in India. With medical costs rising steadily every year, having the right health insurance policy is essential to protect yourself and your loved ones from unexpected expenses. However, choosing the correct health insurance plan can feel overwhelming because of the vast array of policies and terms available. This detailed guide will walk you through the process step by step, helping you make an informed decision.

Why Health Insurance is Crucial in India

India’s healthcare system is a mix of public and private providers. While government hospitals provide affordable healthcare, they often suffer from overcrowding, long waiting times, and limited access to advanced treatments. Private hospitals offer superior infrastructure and quicker service but come with high treatment costs.

For many Indian families, even a single hospitalization can lead to financial hardship or debt. Health insurance acts as a safety net by covering medical expenses such as hospital stays, surgeries, doctor fees, medicines, and diagnostic tests. It ensures that you can seek timely treatment without worrying about the cost, which is especially important in emergency situations.

Furthermore, health insurance encourages preventive care, which helps detect diseases early and avoid expensive complications later. The Insurance Regulatory and Development Authority of India (IRDAI) plays a vital role by regulating insurance companies and ensuring consumer protection through clear guidelines and policy transparency.

Types of Health Insurance Policies in India

Understanding the different types of health insurance plans available will help you pick the one best suited to your needs.

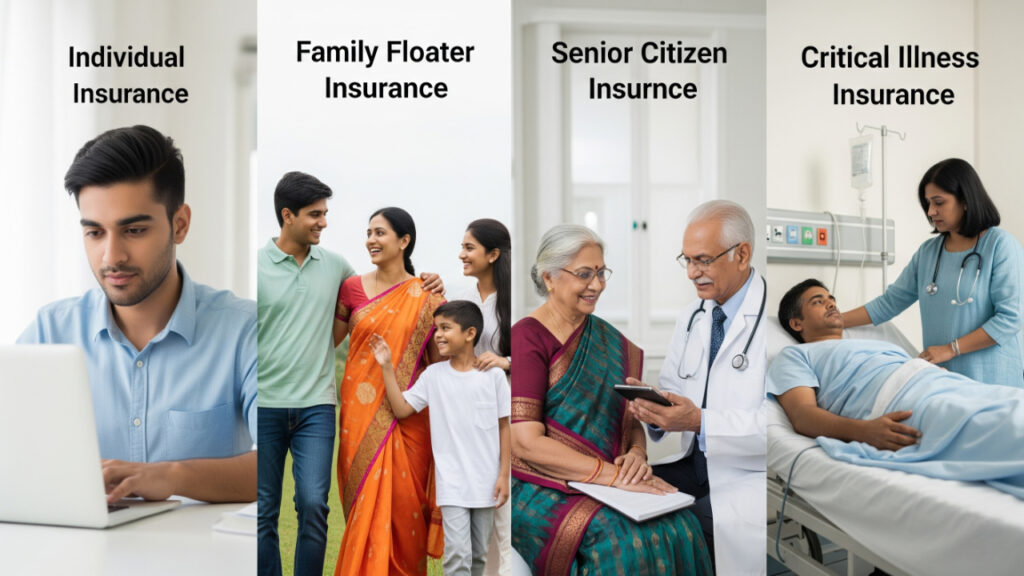

Individual Health Insurance

An individual health insurance policy covers only one person—the policyholder. The sum insured (the maximum amount payable by the insurer in a policy year) is exclusive to that individual and cannot be shared with others. This type of policy is ideal for young, single individuals who do not have dependents. It allows you to customize coverage according to your personal health risks and budget.

Family Floater Policy

A family floater plan is designed to cover multiple family members under a single sum insured. It generally includes the insured person, their spouse, dependent children, and sometimes parents. All insured members share the total coverage limit. For example, if the sum insured is ₹10 lakhs, any claim made by a family member reduces the available amount for others. Family floaters are cost-effective for young families as the premium is usually lower than buying individual plans for each member.

Senior Citizen Health Insurance

Health risks tend to increase with age, making health insurance vital for people above 60 years. Senior citizen policies are tailored to provide coverage for age-related ailments and pre-existing conditions with relatively higher sum insured options. However, these plans come with higher premiums and may have longer waiting periods. They also include benefits such as home healthcare services and specialized hospitalization coverage for elderly diseases.

Critical Illness Insurance

This policy type focuses specifically on serious illnesses such as cancer, heart attacks, strokes, and kidney failures. It provides a lump sum payout upon diagnosis, which can be used for treatment or any other expenses. Critical illness plans can be standalone or added as riders to existing health insurance policies. They help cover costs that may not be included in regular hospitalization plans, such as chemotherapy or long-term rehabilitation.

Top-Up and Super Top-Up Plans

Top-up plans offer additional coverage beyond the basic health insurance limit. Once your base plan’s coverage is exhausted, the top-up plan kicks in to cover further expenses up to the top-up limit. Super top-up plans are more flexible as they consider the total medical expenses incurred over a policy year, not just per hospitalization. These plans are ideal if you want to extend your coverage without paying high premiums for a large base sum insured.

Government-Backed Health Schemes

Recognizing the importance of health security for economically weaker sections, the government of India launched schemes like Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana (PM-JAY) which provides coverage up to ₹5 lakhs per family annually. Similarly, the Employees’ State Insurance Scheme (ESIS) covers salaried employees earning below a certain threshold. These schemes are designed to ensure access to affordable healthcare for millions but may have limitations on hospital choice and coverage scope compared to private plans.

Assessing Personal Needs Before Choosing a Health Insurance Policy

Before selecting a health insurance plan, it’s crucial to analyze your own circumstances and needs in detail.

Age and Health Status

Younger individuals generally have fewer health issues and can get comprehensive insurance at a lower cost. On the other hand, as you age or develop chronic illnesses such as diabetes or hypertension, premiums increase, and the number of insurers willing to cover you may reduce. If you have any pre-existing diseases, look for plans with shorter waiting periods or specialized coverage for these conditions.

Family Composition

Your family structure significantly influences the type of health insurance you need. A single person might opt for an individual plan, but a nuclear family with parents and children is better served by a family floater policy. If you have elderly parents who require frequent medical attention, consider a separate senior citizen policy as part of your overall health coverage.

Location and Medical Costs

Healthcare costs vary greatly depending on where you live. Treatment in metropolitan cities such as Delhi, Mumbai, or Bangalore can be significantly costlier than in smaller towns. Therefore, when choosing your sum insured and plan benefits, factor in local hospital costs and availability of network hospitals in your city.

Budget and Premium Affordability

While it might be tempting to select a high sum insured, you must balance coverage with what you can afford in premiums. Use online health insurance premium calculators to estimate costs based on your age, sum insured, and plan type. Remember that the goal is to have adequate protection without stretching your finances.

Critical Features to Evaluate in a Health Insurance Plan

Choosing the right policy involves more than just looking at the premium and sum insured. Here are some features you should carefully evaluate:

Sum Insured

The sum insured represents the maximum amount your insurer will pay during a policy year. Considering the high costs of hospitalization and surgeries in India, especially in private hospitals, choosing a sufficient sum insured is vital. For individuals living in metro cities, at least ₹10–15 lakhs is recommended. For families, coverage should ideally start at ₹20 lakhs or higher, depending on family size and medical history.

Cashless Network Hospitals

Insurance providers have tie-ups with a network of hospitals where you can avail cashless treatment. This means the insurer settles the hospital bills directly, and you do not need to pay out-of-pocket upfront. It’s important to check if the insurer has a wide network of hospitals near your residence or workplace, as this adds convenience and reduces hassle during emergencies.

Pre and Post-Hospitalization Coverage

Medical expenses do not end the moment you are discharged. Tests and medications before and after hospitalization can be costly. Good health insurance policies cover expenses incurred for a specified number of days before and after hospital stays—usually 30 days before and 60 to 90 days post-discharge. This coverage ensures you are protected from additional out-of-pocket expenses.

Maternity Benefits and Newborn Cover

If you are planning to start or expand your family, consider policies that include maternity benefits. These typically cover delivery charges, prenatal and postnatal care, and vaccinations for the newborn. Such benefits often come with waiting periods ranging from 2 to 4 years, so plan accordingly.

Co-Payment Clause

Some insurance policies include a co-payment clause where the insured must bear a certain percentage of the medical expenses. For instance, if the co-pay is 20%, you pay 20% of the hospital bill and the insurer pays the rest. While this reduces premiums, it can be a burden during expensive treatments. It is advisable to avoid plans with high co-payment clauses, especially for senior citizens or individuals with chronic illnesses.

No Claim Bonus (NCB)

NCB is a valuable benefit that rewards policyholders for not making claims during a policy year. Many insurers increase the sum insured by a percentage (often 5-10%) for every claim-free year, sometimes doubling the sum insured over 4 to 5 years without extra premium. This encourages policyholders to maintain good health and avoid unnecessary claims.

Daycare Treatments and OPD Coverage

Advancements in medical technology have made many treatments possible without 24-hour hospitalization. Daycare procedures such as chemotherapy, dialysis, cataract surgery, or minor surgeries are now common. Ensure that your policy covers these procedures.

Some policies also offer OPD (Outpatient Department) coverage, which reimburses expenses for doctor visits, medicines, and diagnostics without hospital admission. This is beneficial for chronic disease management but is usually available at an additional cost.

Choosing Between Public vs. Private Insurance Providers

India offers health insurance from both government-backed schemes and private companies. Each has its own advantages and limitations.

Government schemes like Ayushman Bharat (PM-JAY) and ESIC provide affordable or even free coverage to millions of Indians, especially from economically weaker sections. These schemes have wide reach but may have limited hospital networks and less flexibility in terms of coverage options. Additionally, claim settlement times may be longer compared to private insurers.

Private insurers, on the other hand, offer a variety of customizable plans, wider hospital networks, and faster claim processing. Private policies usually provide better customer service, more add-on benefits, and more competitive claim settlement ratios. When choosing a private insurer, reviewing their claim settlement ratio (CSR) is critical as it indicates how many claims were successfully paid out of total claims filed.

Where to Buy Health Insurance in India

Health insurance policies can be purchased through multiple channels.

One option is to buy directly from insurance company websites such as HDFC ERGO, Star Health, or Niva Bupa. These portals offer detailed information on plans and online purchase facilities.

Alternatively, insurance aggregator platforms like Policybazaar, Coverfox, and Turtlemint enable you to compare multiple insurers and policies side-by-side. They also provide premium calculators, customer reviews, and assistance with policy purchase and claim processes.

You can also buy through banks or offline agents, but it is advisable to choose a method that offers transparent information and good after-sales service.

Tax Benefits of Health Insurance under Section 80D

Health insurance premiums paid by an individual are eligible for tax deductions under Section 80D of the Income Tax Act. This benefit encourages people to invest in health insurance.

For self, spouse, and dependent children, you can claim deductions up to ₹25,000 annually. If you pay premiums for your parents’ health insurance, an additional deduction of ₹25,000 (₹50,000 if parents are senior citizens) can be claimed. This reduces your taxable income, leading to savings in income tax.

Understanding this benefit is essential as it makes health insurance a financially attractive option beyond just health protection.

Reading the Policy Document Carefully

The policy document is the legal contract between you and the insurer. It is vital to read it carefully before signing up. Focus on sections detailing policy exclusions, waiting periods, claim procedures, and renewal terms.

Policy exclusions list treatments and conditions that are not covered. Common exclusions include cosmetic surgeries, experimental treatments, dental procedures, or injuries due to risky activities. Waiting periods specify the duration for which coverage is not applicable on certain conditions, often 2-4 years for pre-existing diseases.

Understanding room rent limits is also important. Some policies cap the reimbursement amount for hospital room rent, and exceeding this limit could increase your out-of-pocket expenses.

Conclusion

Choosing the right health insurance policy is a critical step toward securing your and your family’s health and financial future. It requires careful assessment of your personal circumstances, thorough understanding of policy features, and comparison of available options.

Start early, consider your family’s health needs, budget realistically, and prioritize policies with comprehensive coverage and good claim records. Use trusted online platforms like Policybazaar or consult certified insurance advisors for personalized guidance.

Remember, the right health insurance policy not only protects your health but also safeguards your wealth from unexpected medical expenses.

FAQs

Q1: What is the best age to buy health insurance in India?

A: The best age is early 20s to early 30s when premiums are lower and health risks are minimal. Buying young also helps avoid waiting periods for pre-existing conditions.

Q2: Is employer-provided health insurance sufficient?

A: Employer insurance is helpful but often limited to the job tenure and may have lower sum insured. Having a personal policy ensures continuous coverage.

Q3: Are COVID-19 treatments covered under health insurance?

A: Yes, IRDAI has mandated that all health insurance policies cover COVID-19 related hospitalization and treatment.

Q4: Can I switch health insurance providers without losing benefits?

A: Yes, policy portability allows switching insurers while carrying forward waiting periods and No Claim Bonus.

Q5: Are AYUSH treatments covered?

A: Many insurers now include coverage for Ayurveda, Yoga, Naturopathy, Unani, Siddha, and Homeopathy treatments in their policies.

Q6: Can NRIs buy health insurance in India?

A: Yes, NRIs can purchase Indian health insurance policies but coverage is usually restricted to treatment within India.

Q7: What documents do I need for making a health insurance claim?

A: Commonly required documents include hospital bills, discharge summaries, prescriptions, diagnostic reports, and a valid identity proof.

Q8: Can I get insurance if I have chronic diseases?

A: Yes, but you may have to undergo medical tests, and a waiting period of 2-4 years typically applies before coverage starts for those conditions.

Q9: How often should I review my health insurance policy?

A: It’s advisable to review annually or after major life changes such as marriage, childbirth, or diagnosis of new health conditions.

Q10: Is buying health insurance online safe?

A: Yes, buying through IRDAI-registered portals like Policybazaar and Coverfox is safe, transparent, and convenient.