by

by In today’s fast-paced world, financial needs can arise unexpectedly. Whether it is a medical emergency, education expense, home renovation, or an urgent travel plan, personal loans provide a quick and flexible solution. With the rise of digital banking and fintech platforms in India, applying for a personal loan online has become a simple and convenient option. This guide will walk you through everything you need to know about how to apply for a personal loan online in India, including eligibility criteria, required documents, steps to apply, and tips to get the best deal.

What is a Personal Loan?

A personal loan is an unsecured loan provided by banks or Non-Banking Financial Companies (NBFCs) without requiring collateral such as property or assets. This means you can borrow a specific amount of money based on your repayment capacity, which you must pay back with interest over a fixed tenure. The interest rates for personal loans vary widely depending on factors like credit score, income, and lender policies, typically ranging from 10% to 24% per annum.

Because it is an unsecured loan, lenders assess your eligibility primarily based on your credit history and financial standing. The advantage of a personal loan is the flexibility to use it for any purpose, unlike home or car loans which are tied to specific assets.

Why Apply for a Personal Loan Online?

Applying for a personal loan online saves time, effort, and reduces paperwork compared to traditional offline methods. Here are some key advantages:

- Convenience: You can apply from anywhere at any time without visiting the bank branch.

- Faster Processing: Many lenders offer instant eligibility checks and quick loan approvals online.

- Transparency: Online platforms provide clear information about interest rates, fees, and tenure options.

- Multiple Options: You can compare various lenders on aggregators like BankBazaar or Paisabazaar to find the best deal.

These benefits make online personal loans the preferred choice for millions of Indians today.

Step-by-Step Process: How to Apply for a Personal Loan Online in India

1. Check Your Eligibility

Before starting your application, verify if you meet the lender’s eligibility criteria. Although requirements vary slightly among banks and NBFCs, most lenders expect:

- Applicant age between 21 and 60 years

- Minimum monthly income as per lender norms (usually ₹15,000 to ₹30,000)

- Stable employment with at least 1-2 years of continuous income

- A good credit score, typically 750 or above

You can check your credit score and report for free on sites like CIBIL or Experian India. A good credit score significantly improves your chances of approval and may fetch you lower interest rates.

2. Research and Compare Loan Offers

India has a large number of personal loan providers including reputed banks such as HDFC Bank, ICICI Bank, State Bank of India, and NBFCs like Bajaj Finserv and Tata Capital.

Each lender differs in interest rates, processing fees, prepayment options, loan tenure, and eligibility requirements. You should compare these features carefully using online marketplaces such as BankBazaar or Paisabazaar, which allow side-by-side comparisons. This helps you select the loan best suited to your financial needs.

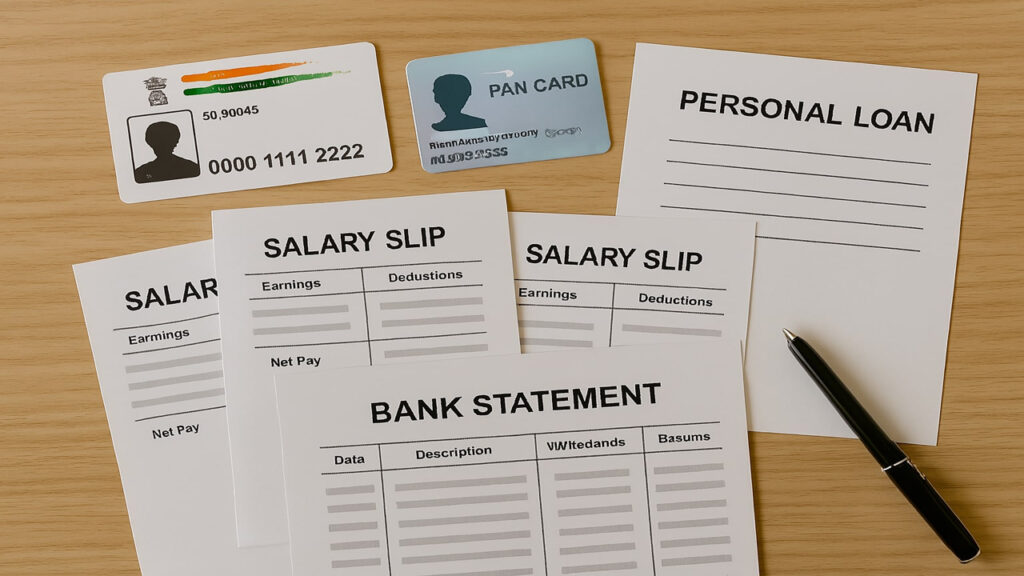

3. Prepare the Necessary Documents

The next step involves collecting the documents required for the loan application and verification. These generally include:

- Proof of Identity: Aadhaar card, PAN card, Passport, or Voter ID

- Proof of Address: Utility bill, Aadhaar, Passport, or Ration Card

- Income Proof: Latest salary slips (usually last 3 months), Income Tax Returns (ITR), or bank statements (last 6 months)

- Photograph: Recent passport-sized photo

- Bank Account Details: Cancelled cheque or bank statement for loan disbursal

Some lenders offer simplified documentation for salaried employees or existing customers. Others might also verify your Aadhaar electronically using e-KYC, speeding up the process.

4. Fill Out the Online Application Form

Once you’ve chosen a lender, visit their official website or use a trusted loan aggregator platform. You will be required to fill in personal details such as:

- Full name, date of birth, and contact details

- Employment type (salaried or self-employed) and monthly income

- Desired loan amount and tenure

- Bank account number for disbursal

Many platforms allow you to check eligibility instantly by entering basic details before proceeding.

5. Upload Documents and Complete Verification

After submitting the application form, upload scanned copies or photographs of your documents. The lender will then verify your identity, address, and income. Some banks use video KYC or OTP-based Aadhaar verification to complete this step digitally, avoiding the need for physical document submission.

6. Loan Approval and Disbursal

If your documents are in order and creditworthiness is satisfactory, the lender will approve your loan application. You will receive an approval message via SMS or email along with the loan amount, interest rate, tenure, and EMI details.

Once you accept the loan offer, the funds are typically credited directly to your bank account within 24 to 48 hours, though some lenders offer instant disbursal for pre-approved customers.

Important Factors to Consider While Applying Online

Interest Rate and Processing Fees

The interest rate is the cost you pay to borrow the loan. Personal loan interest rates in India fluctuate based on your credit profile and lender policies. Besides interest, you may also pay a one-time processing fee, usually 1-2% of the loan amount. Always check for hidden charges before finalizing.

Loan Tenure and EMI

Personal loans can be taken for short to medium terms, usually from 12 to 60 months. A longer tenure means lower monthly EMIs but higher overall interest paid. Calculate your monthly repayment ability carefully before selecting the tenure.

Prepayment and Foreclosure Charges

If you plan to repay your loan early, check whether the lender allows prepayment or foreclosure and if any penalty fees apply. Some lenders offer no prepayment charges, which can save money on interest.

Common Mistakes to Avoid When Applying for a Personal Loan Online

- Applying to multiple lenders simultaneously, which can negatively affect your credit score due to multiple credit inquiries

- Submitting incomplete or incorrect documents causing delays or rejection

- Ignoring the fine print regarding interest rates, fees, and prepayment options

- Not comparing offers and blindly accepting the first loan offer received

Conclusion

Applying for a personal loan online in India is a convenient and efficient way to meet urgent financial needs without collateral. By following the steps of checking your eligibility, comparing loan options, preparing documents, and submitting an accurate online application, you can get your loan approved quickly and with minimal hassle.

For beginners, starting with trusted banking websites or using reputed loan marketplaces like BankBazaar or Paisabazaar can make the entire process easier and more transparent. Remember to maintain a good credit score and repay EMIs on time to improve your borrowing power for future needs.

FAQs

Q1: What is a personal loan?

A: A personal loan is an unsecured loan provided by banks or NBFCs without requiring collateral. It can be used for various personal needs such as medical emergencies, education, travel, or debt consolidation.

Q2: What is the eligibility criteria for a personal loan in India?

A: Typically, borrowers must be between 21 to 60 years old, have a stable income (usually ₹15,000+ monthly), a good credit score (750+), and at least 1-2 years of continuous employment or income.

Q3: What documents are required to apply for a personal loan online?

A: You will generally need identity proof (Aadhaar, PAN, Passport), address proof (utility bill, Aadhaar), income proof (salary slips, IT returns), a recent photograph, and bank account details.

Q4: How long does it take to get a personal loan disbursed online?

A: Most lenders disburse the loan amount within 24 to 48 hours after approval, provided all documents are verified and complete.

Q5: Can I apply for a personal loan online without visiting the bank?

A: Yes, the entire process from application to disbursal can be completed online through bank or NBFC websites or through third-party loan aggregator platforms.

Q6: What are the typical interest rates for personal loans in India?

A: Interest rates usually range from 10% to 24% per annum and depend on factors like your credit score, income, and lender policies.

Q7: Is there a penalty for prepaying or foreclosing a personal loan early?

A: Some lenders may charge a prepayment or foreclosure fee. It’s important to check these charges before applying if you plan to repay early.

Q8: Will applying to multiple lenders affect my credit score?

A: Yes, multiple loan applications within a short period can lower your credit score. It is advisable to research and choose lenders carefully before applying.

Q9: How can I compare personal loan offers online?

A: You can use online loan comparison platforms like BankBazaar, PaisaBazaar, or lender websites to compare interest rates, processing fees, tenure, and other terms.

Q10: What should I be cautious about while applying for a personal loan online?

A: Avoid submitting incomplete or incorrect documents, check all loan terms carefully, avoid multiple simultaneous applications, and choose a loan tenure that fits your repayment capacity.