by

by Getting a credit card is no longer just for the wealthy or high-salaried individuals. With the rise of digital banking and inclusive financial services, it’s now easier than ever to apply for a credit card online in India with low income. Whether you’re a student, a young professional earning a modest salary, or someone building credit for the first time, banks and fintech platforms today offer simple and accessible credit solutions designed just for you.

This article explains in detail how you can apply for a credit card online even if your monthly income is as low as ₹10,000. We’ll explore the eligibility criteria, the best credit card options for low-income users, the application process, required documents, and tips to ensure approval—all written in beginner-friendly language.

Understanding the Credit Card Landscape in India

Until a few years ago, applying for a credit card required a high income, strong credit history, and lengthy paperwork. But in recent years, banks like SBI, Kotak Mahindra, Axis Bank, and ICICI, along with new-age fintech platforms like Slice, OneCard, and UNI, have made the process far more inclusive.

Now, even individuals with low or no credit history and incomes starting at ₹10,000 per month can apply for credit cards online. There are specific products created for this segment, such as secured credit cards, student cards, and entry-level cards with low documentation requirements.

These cards allow users to build credit history, enjoy cashbacks and offers, manage monthly spending, and handle small emergencies—all while giving access to formal credit systems in a responsible manner.

Who Can Apply with Low Income?

To apply for a credit card online in India with a low income, you must still meet some basic eligibility criteria. While these vary slightly from bank to bank, most institutions follow these common standards:

- You must be at least 18 years of age, though some banks prefer applicants over 21.

- You should have a monthly income of at least ₹10,000 to ₹15,000 for entry-level unsecured cards. If not, you can apply for a secured card.

- You need valid documents such as PAN card, Aadhaar card, and a photograph.

- A basic credit score is preferred for unsecured cards, though not mandatory for secured options.

Secured credit cards don’t require income proof at all and are backed by a fixed deposit. These are perfect for students, part-time workers, and individuals with irregular income sources.

Best Credit Card Options for Low-Income Individuals

If you’re applying with limited income, it’s important to pick a card that suits your financial profile. There are two major types of cards you can consider:

Secured Credit Cards are issued against a fixed deposit. This means you don’t need to show salary slips or bank statements. The bank holds your FD as collateral and offers a credit limit of around 80–90% of that amount. Popular options include the Kotak 811 #DreamDifferent Card, SBI Unnati Card, and Axis Insta Easy Card.

Unsecured Credit Cards for Low Income are suitable for salaried individuals earning ₹10,000–₹20,000 per month. These cards don’t need a fixed deposit but require income proof. Examples include SBI SimplyCLICK, AU Bank Altura Card, and ICICI Platinum Chip Card.

Each of these cards comes with digital application processes, quick approvals, and basic reward programs.

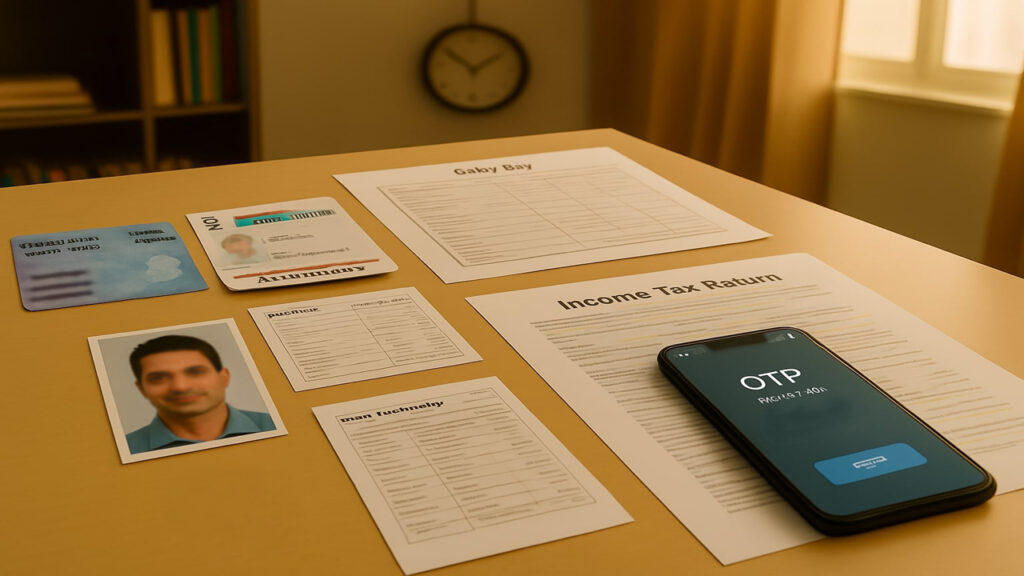

Required Documents for Online Application

While secured cards require minimal documents, unsecured cards still need standard identification and income documents.

For all cards, you must provide:

- Your PAN card

- Aadhaar card (linked with mobile for OTP)

- A passport-sized photograph

For unsecured cards, banks may ask for:

- Latest 3-month salary slips

- Bank statements showing salary credits

- Latest ITR (Income Tax Return) or Form 16

Make sure the documents are clear, up to date, and match the information you provide on the application form.

Step-by-Step Process to Apply Online

The application process for a credit card online in India is fully digital and takes just a few minutes if your documents are ready.

First, visit the official website of the bank or a trusted comparison platform like Paisabazaar or BankBazaar. Use the eligibility checker to see which cards you qualify for based on your age, income, and job profile.

Once you choose a suitable card, click on “Apply Now” and begin filling in your personal details—name, address, date of birth, PAN, mobile number, and email. You’ll also be asked about your employment type, monthly income, and office details.

Next, upload the required documents. For e-KYC, you’ll receive an OTP on your Aadhaar-linked mobile number. Some banks may also ask for a short video KYC, where you show your PAN and Aadhaar on camera for identity verification.

After successful submission, you’ll receive an application ID. You can use this to track your application. Most banks provide a decision within 24–72 hours. If approved, a virtual card may be activated instantly. The physical card is usually delivered to your address within 5 to 10 working days.

How to Improve Your Chances of Approval

To increase your chances of getting approved, apply for a card that matches your income level. If you are unsure, start with a secured card, which almost guarantees approval.

Make sure your documents are complete and accurate. Avoid applying for multiple cards at once, as it creates multiple hard inquiries on your credit report and reduces your score. Also, if you already have a salary account with the bank, apply through that bank for better approval chances.

Finally, if your credit score is low or if you’ve been rejected before, wait at least 90 days, improve your score, and then reapply.

How to Use Your Credit Card Responsibly

Once you get your card, start using it wisely. Use it for small purchases like groceries, phone recharges, or utility bills. Always pay your full bill before the due date to avoid interest charges. Don’t just pay the “minimum due”—this leads to high interest and debt.

Keep your usage below 30–40% of your credit limit. If your limit is ₹10,000, don’t spend more than ₹3,000 to ₹4,000 per month. This helps build a strong credit score. Over time, with good usage, you can apply for better cards with higher limits and richer rewards.

Final Thoughts

If you’ve been thinking about how to apply for a credit card online in India with low income, the process today is simpler, safer, and more accessible than ever. Thanks to secured and low-income cards, anyone with basic KYC documents and financial discipline can enjoy the convenience of digital payments, rewards, and improved creditworthiness.

Start small, use your card wisely, and you’ll open the door to better financial opportunities in the future.

FAQs

Q1: Can I get a credit card if my income is below ₹15,000?

A: Yes, you can get a secured credit card or even some unsecured entry-level cards depending on your profile.

Q2: What is a secured credit card?

A: A secured credit card is issued against a fixed deposit and does not require income proof or credit history.

Q3: Do I need a job to apply for a credit card?

A: Not necessarily. If you have a fixed deposit, you can get a secured card without a job or income.

Q4: Can I apply for a credit card with no credit score?

A: Yes, secured credit cards are great for building credit from scratch.

Q5: Is applying for a credit card online safe?

A: Yes, as long as you apply through official bank websites or verified financial platforms.

Q6: How long does the application process take?

A: The online form takes about 10–15 minutes, and approvals typically take 1 to 3 working days.

Q7: What if my application gets rejected?

A: You can check the reason, fix it (like improving your score), and apply again after a few months.

Q8: Which is better—secured or unsecured credit cards?

A: For beginners or low-income individuals, secured cards are safer and easier to get approved for.

Q9: Will using my card increase my credit score?

A: Yes, regular and timely usage helps build your credit score over time.

Q10: Are there zero-fee credit cards for low-income users?

A: Yes, some secured cards like SBI Unnati have no annual fee for the first four years.